Kate Wood is a mortgages and student loans writer and spokesperson who joined NerdWallet in 2019. With an educational background in sociology, Kate feels strongly about issues like inequality in homeownership and higher education, and relishes any opportunity to demystify government programs. Prior to joining NerdWallet, she wrote about home remodeling, decor and maintenance for This Old House magazine.

Reviewed by Michael Soon Lee Michael Soon Lee

Business expert Michael Soon Lee, Ph.D., is an internationally recognized speaker and consultant whose clients include Coca-Cola, Chevron, Boeing, State Farm Insurance and General Motors. He is the author of nine books, including "Black Belt Negotiating” and "Cross-Cultural Selling for Dummies.” Michael has been an award-winning real estate broker since 1980, was licensed to practice taxation before the Internal Revenue Service and is a former certified financial planner who taught taxation for the College for Financial Planning. His articles have appeared in newspapers and magazines such as The Wall Street Journal, the San Francisco Chronicle, the Los Angeles Times and Consumer Reports. He was dean of the School of Management at John F. Kennedy University and served as an adjunct faculty member for Golden Gate University for over 20 years.

At NerdWallet, our content goes through a rigorous editorial review process. We have such confidence in our accurate and useful content that we let outside experts inspect our work.

Assigning Editor Alice HolbrookAlice Holbrook is a former editor of homebuying content at NerdWallet. She has covered personal finance topics for almost a decade and previously worked on NerdWallet's banking and insurance teams, as well as doing a stint on the copy desk. She is based in Ann Arbor, Michigan.

Fact Checked Co-written by Taylor Getler Taylor Getler

Writer | Home equity, first-time home buying, home warranties

Taylor Getler is a home and mortgages writer for NerdWallet. Her work has been featured in outlets such as MarketWatch, Yahoo Finance, MSN and Nasdaq. Taylor is enthusiastic about financial literacy and helping consumers make smart, informed choices with their money.

Some or all of the mortgage lenders featured on our site are advertising partners of NerdWallet, but this does not influence our evaluations, lender star ratings or the order in which lenders are listed on the page. Our opinions are our own. Here is a list of our partners.

A home equity line of credit, or HELOC, is a second mortgage that gives you access to cash based on the value of your home. (It can also be a primary mortgage if you own your home outright.) You borrow against your equity, which is the home’s value minus the amount you owe on the primary mortgage. You can usually borrow up to 85% of your equity, though this varies by lender.

You can draw from a home equity line of credit and repay all or some of it monthly, somewhat like a credit card. Unlike a credit card, however, HELOCs are not intended for minor expenses.

When you’re shopping around for a loan, borrowing from the equity in your home will often get you the best rate.

HELOC & Home Equity Loans from our partners

Home Equity Loans Check RateNerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score Max loan amount Check Rate

on New American Funding

New American Funding

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score Max loan amount Check Rateon New American Funding

on Bethpage Federal Credit Union

Bethpage Federal Credit Union

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score Max loan amount Check Rateon Bethpage Federal Credit Union

on New American Funding

New American Funding

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score Max loan amount Check Rateon New American Funding

Check RateNerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score Max loan amount Check Rate Check Rateon Rocket Mortgage

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

NerdWallet's ratings are determined by our editorial team. The scoring formula incorporates coverage options, customer experience, customizability, cost and more.

Min. credit score Max loan amount Check Rateon Rocket Mortgage

COMPARE MORE LENDERSA HELOC allows you to borrow cash from the value of your home — preferably for wealth-building expenditures, such as home improvements.

Most HELOC lenders will let you borrow up to 85% of the value of your home (minus what you owe), though some have higher or lower limits.

You typically have 10 years to withdraw cash from a home equity line of credit, while paying back only interest, and then 20 more years to pay back your principal plus interest at a variable rate.

In order to qualify, lenders usually want you to have a credit score over 620, a debt-to-income ratio below 40% and equity of at least 15%.

Rates vary by lender, and the annual percentage rate, or APR, that you’re offered depends largely on factors such as:

Your credit score. Your existing debt. The amount you wish to borrow.Most HELOC rates are indexed to a base rate called the prime rate, which is the lowest credit rate lenders are willing to offer their most attractive borrowers.

Lenders consider a borrower’s profile and add a margin to the prime rate to calculate a rate offer. For example, if a lender applies a margin of 1.5% to a prime rate of 8.5%, that borrower’s rate will be 10%.

Sometimes a lender may add a negative margin. A lender may do this as part of an introductory offer to attract borrowers before switching to a positive margin later in the life of the loan.

Current prime rate

Prime rate last week

Prime rate in the past year — low

Prime rate in the past year — high

Most HELOCs have adjustable interest rates. This means that as baseline interest rates go up or down, the interest rate on your HELOC will adjust, too. However, because a HELOC is secured against the value of your home, the interest is typically lower than the rate you’d pay on a credit card or personal loan, and closer to a mortgage rate.

Shop around with at least three lenders when looking for the best HELOC rate. Check your bank or mortgage provider; it might offer discounts to existing customers. Also, take note of introductory offers like initial rates that will expire at the end of a given term.

Before you open a HELOC, you might look for lenders that offer a fixed-rate option . This lets you lock in your APR when you draw from your equity, which protects your loan from rising interest rates and can make long-term financial planning a little easier.

A HELOC gives you the flexibility to borrow against your home equity, repay and repeat. Because HELOCs are secured by an asset — your home — interest rates are typically competitive. This also makes them risky, because you can lose your home if you cannot make your payments.

There are two phases of a HELOC:

The draw period , when you can borrow money from the account, up to your approved limit. You have to make interest payments, but payments towards the principal are optional. This period typically lasts 10 years.

The repayment period , when you can’t take out more money and have to make both principal and interest payments until you’ve paid off what you’ve borrowed. With the addition of principal, the monthly payments can rise sharply compared with the draw period. The length of the repayment period varies; it’s often 20 years.

You’ll have a few options to withdraw money from this account. You can access it via online transfer or with a bank card at an ATM or point of sale (the same as you would with a debit card), or you can write checks from the account if the lender issues them.

In addition to interest, there are further costs to consider before taking out a HELOC.

Closing costs , which are often between 2% and 5% of the loan amount. Some lenders don’t charge closing costs at all, but be aware that this can be contingent on keeping the line open for a certain amount of time.

Annual fees. Some lenders charge annual fees for HELOC customers, which are often around $50 per year.

Lender requirements will vary, but here's what you'll generally need to get a HELOC:

A debt-to-income ratio that's 40% or less. A credit score of 620 or higher. A home value that’s at least 15% more than you owe.The process of getting a HELOC is similar to that of applying for a purchase or refinance mortgage. You’ll provide some of the same documentation and demonstrate that you’re creditworthy. Here are the steps you’ll follow:

Calculate your existing equity (the current value of your home, minus what you owe) and decide how much you need to borrow.

Gather the necessary documentation (such as W-2s, recent pay stubs, mortgage statements and personal identification) before you apply so the process will go smoothly.

Shop around multiple lenders and apply for the HELOC.Read your disclosure documents carefully and ask the lender questions. Make sure the HELOC will fit your needs. For example, does it require you to borrow thousands of dollars upfront (often called an initial draw)? Do you have to open a separate bank account to get the best rate on the HELOC?

Be aware that the underwriting process, though not as extensive as when you got your mortgage, can take weeks.

Await loan closing, when you sign paperwork and the line of credit becomes available.Don't assume the price you paid at closing is what your home is worth today. During underwriting, your lender may order an appraisal to confirm the home's value. If home prices in your area have appreciated while you've owned your home, you'll also have more equity because the difference between the property's higher value and the amount remaining on your mortgage will be larger.

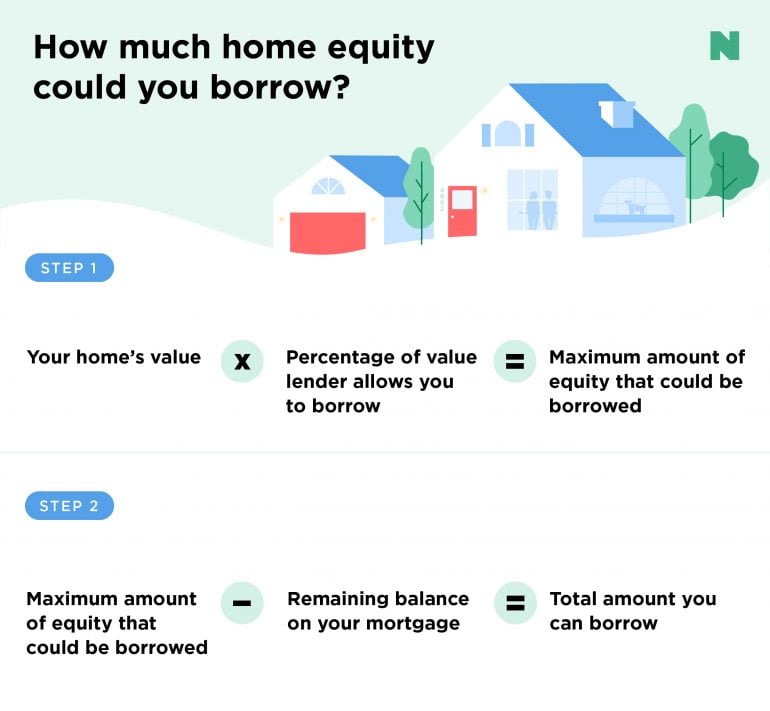

The maximum amount of your home equity line of credit will vary based on the value of your home, what percentage of that value the lender will allow you to borrow against and how much you owe on your mortgage. Two quick calculations can give you an idea of what you might be able to borrow with a HELOC.

Your home's current value x Percentage of value the lender allows you to borrow = Maximum amount of equity that could be borrowed

Maximum amount of equity that could be borrowed - Remaining balance on your mortgage = Total amount you can borrow

Say you have a home worth $300,000 with a balance of $200,000 on your first mortgage and your lender will allow you to access up to 85% of your home’s value. Multiplying the home's value ($300,000) by the percentage the lender will allow you to borrow (85%, or 0.85) gives you a maximum amount of $255,000 in equity that could be borrowed. Subtract the amount you still owe on your mortgage ($200,000) to get the total amount you can borrow with a HELOC — $55,000.

Or skip doing the math, and use the HELOC calculator below to see how much you might be able to borrow.

Whether a home equity line of credit is a good idea really comes down to your goals and financial situation.

The interest on your HELOC may be tax-deductible if you use the money to buy, build or substantially improve your home, and the combination of the HELOC and your mortgage don't exceed stated loan limits, according to the IRS.

A HELOC is not recommended if your income is unstable or if you won’t be able to afford payments if interest rates rise.

It may not be the best choice if you’re planning to move soon. One of the main benefits of a HELOC is its long borrowing and payment timeline, and you’ll have to pay it off entirely at the time of sale.

A HELOC may also not be the right choice if you aren’t looking to borrow much money (in which case the costs may not be worth it, and you should consider a low interest credit card instead), or if you intend to use it for basic needs, small purchases or expenses that don’t build personal wealth (like a new car or vacation).

That depends on your financial situation and needs. A HELOC behaves like a revolving line of credit, letting you tap your home’s value in the amount you need as you need it. A home equity loan works more like a conventional loan, with a lump-sum withdrawal that is paid back in installments.

HELOCs typically have variable interest rates, while home equity loans are usually issued with a fixed interest rate. This can save you from a future payment shock if interest rates rise. Work with your lender to decide which option is best for your financing needs.

Because most HELOCs have an adjustable rate, it’s possible your payments could exceed what you’d originally planned. If you can’t pay back what you’ve withdrawn, the lender could foreclose on your home; therefore, it’s important to act fast if you foresee a problem. Reach out to the lender to understand your options, and consider refinancing to lower your rate or change your payment terms.

Frequently asked questions What is a HELOC?A home equity line of credit, or HELOC, is a type of second mortgage that lets you borrow against your home equity. Somewhat like with a credit card, you use money from the HELOC as needed and then pay it back over time.

How is a HELOC paid back?A HELOC has two phases, known as the draw period and the repayment period. During the draw period, you borrow money as needed, and required monthly payments generally just cover interest. In the repayment period, you can no longer borrow money, and you'll pay back the principal and interest.

How does a HELOC work?With a HELOC, instead of borrowing a lump sum, you borrow money when you need it. Though your total credit line may be substantial, you pay interest only on the funds you actually use. HELOCs generally have adjustable interest rates, so HELOC rates fluctuate along with the market.

Is HELOC interest tax-deductible?You may be able to claim a tax deduction on your HELOC interest if you used the loan for home improvements. The IRS sets annual limits that vary depending on whether you're single, head of household or filing jointly, and you'll have to itemize your deductions to take advantage of this one.

How does a HELOC affect your credit score?Some bureaus treat HELOCs of a certain size like installment loans rather than revolving lines of credit. This means borrowing 100% of your HELOC limit may not have the same negative effect as maxing out your credit card. Like any line of credit, a new HELOC on your report will likely reduce your credit score temporarily. However, if you borrow responsibly — making timely payments and not utilizing the full credit line — your HELOC could help you build your credit score over time.

What is a HELOC?A home equity line of credit, or HELOC, is a type of

that lets you borrow against your home equity. Somewhat like with a credit card, you use money from the HELOC as needed and then pay it back over time.

How is a HELOC paid back?has two phases, known as the draw period and the repayment period. During the draw period, you borrow money as needed, and required monthly payments generally just cover interest. In the repayment period, you can no longer borrow money, and you'll pay back the principal and interest.

How does a HELOC work?With a HELOC, instead of borrowing a lump sum, you borrow money when you need it. Though your total credit line may be substantial, you pay interest only on the funds you actually use. HELOCs generally have adjustable interest rates, so

fluctuate along with the market.

Is HELOC interest tax-deductible?You may be able to claim a

on your HELOC interest if you used the loan for home improvements. The IRS sets annual limits that vary depending on whether you're single, head of household or filing jointly, and you'll have to itemize your deductions to take advantage of this one.

How does a HELOC affect your credit score?Some bureaus treat HELOCs of a certain size like installment loans rather than revolving lines of credit. This means borrowing 100% of your HELOC limit may not have the same negative effect as maxing out your credit card. Like any line of credit, a new HELOC on your report will likely reduce your credit score temporarily. However, if you borrow responsibly — making timely payments and not utilizing the full credit line — your HELOC could help you build your credit score over time.

About the authorsYou’re following Kate Wood

Visit your My NerdWallet Settings page to see all the writers you're following.

Kate Wood is a mortgages and student loans writer and spokesperson who joined NerdWallet in 2019. With an educational background in sociology, Kate feels strongly about inequality in homeownership and higher education. See full bio.

You’re following Taylor Getler

Visit your My NerdWallet Settings page to see all the writers you're following.

Taylor Getler is a home and mortgages writer for NerdWallet. Her work has been featured in outlets such as MarketWatch, Yahoo Finance, MSN and Nasdaq. Taylor is enthusiastic about financial literacy and helping consumers make smart, informed choices with their money. Email: [email protected]. See full bio.

On a similar note.

Download the app

Disclaimer: NerdWallet strives to keep its information accurate and up to date. This information may be different than what you see when you visit a financial institution, service provider or specific product's site. All financial products, shopping products and services are presented without warranty. When evaluating offers, please review the financial institution's Terms and Conditions. Pre-qualified offers are not binding. If you find discrepancies with your credit score or information from your credit report, please contact TransUnion® directly.

NerdUp by NerdWallet credit card: NerdWallet is not a bank. Bank services provided by Evolve Bank & Trust, member FDIC. The NerdUp by NerdWallet Credit Card is issued by Evolve Bank & Trust pursuant to a license from MasterCard International Inc.

Impact on your credit may vary, as credit scores are independently determined by credit bureaus based on a number of factors including the financial decisions you make with other financial services organizations.

NerdWallet Compare, Inc. NMLS ID# 1617539

California: California Finance Lender loans arranged pursuant to Department of Financial Protection and Innovation Finance Lenders License #60DBO-74812

Insurance Services offered through NerdWallet Insurance Services, Inc. (CA resident license no.OK92033) Insurance Licenses

NerdWallet™ | 55 Hawthorne St. - 10th Floor, San Francisco, CA 94105