The No Surprises Act Section 202(c) of the CAA is focused on enhancing the compensation disclosure rules for group health plans, individual brokers, and consultants. These new disclosure requirements bring group health plans more in-line with the disclosure rules under Section 408(b)(2) of ERISA issued in 2012 that apply to retirement plans (e.g.401(k) plans). This includes all forms of compensation, including standard ongoing compensation, bonuses, finder’s fees, prepaid (advanced) commissions, payments made by third parties, incentive programs not solely related to the plan, etc.

The new ERISA disclosure requirements apply to any covered services provider that reasonably expects to receive $1,000 or more in direct or indirect compensation for brokerage or consulting services provided to an ERISA-covered group health plan.

Amwins Connect has assembled tools and resources to support you with the broker compensation disclosures as well as with communicating the requirement to your clients. View the Nationwide Commission Guide.

In this episode of Coffee with Carriers, Becky Patel, CEO of Amwins Connect, talks with Janet Trautwein, CEO of NAHU. Janet discusses how brokers can comply with the new Compensation Disclosure Requirements while we await further guidance from the Department of Labor.

This applies to both fully insured and self-funded, which included level-funded plans. Non-ERISA plans are not subject to the requirement.

Brokers and consultants (and their subcontractors) for health plans, which include excepted benefits like stand-alone dental and vision, health FSAs, EAPs and HRAs, must disclose, in writing, the amounts on fee disclosure for the plan. The disclosure is required regardless of whether such services will be performed, or such compensation received, by the covered service provider, an affiliate, or a subcontractor. Values can be expressed in the aggregate or by service as a dollar amount, formula, per capita charge for each member, or any other reasonable method with a good faith estimate.

The disclosure descriptions must be sufficient for the client to evaluate ‘reasonableness’. These changes are important for plan sponsors, because any compensation that is deemed ‘unreasonable’ under these new disclosure obligations would likely be a prohibited transaction under ERISA. Prohibited transactions give rise to potential excise taxes and other fiduciary enforcement action.

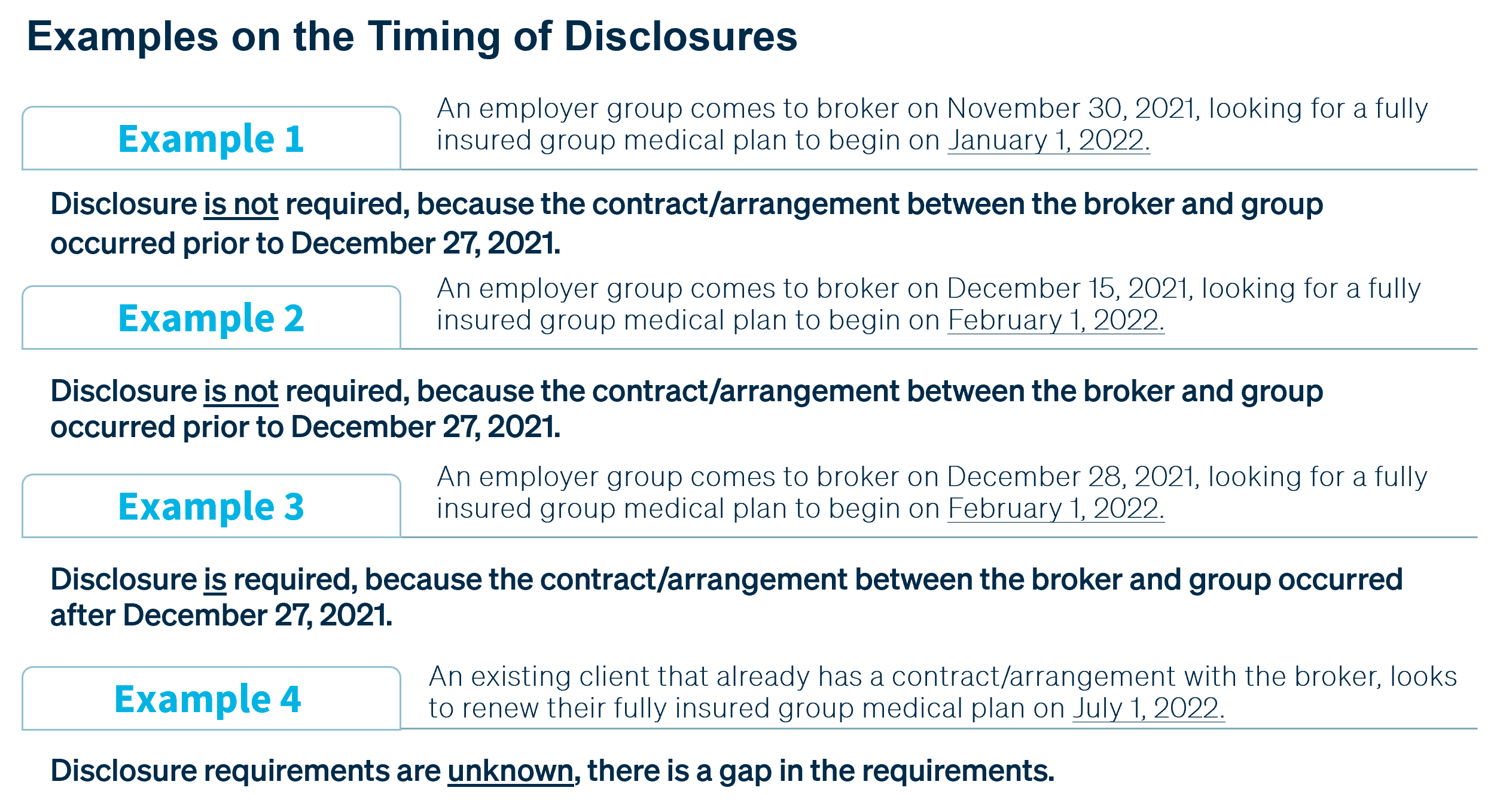

These new fee-disclosure requirements are set to go into effect on December 27, 2021 and were not changed in the most recent FAQs regarding the CAA issued by the Department of Labor, Health and Human Services, and the Treasury on August 20, 2021. On and after December 27, 2021, in order to be considered compliant, a detailed fee disclosure will be required prior to the date the contract or arrangement is entered into, extended or renewed. An updated notice will also be required within 30 days following the discovery of any inadvertent errors or omissions, within 60 days of a compensation change, and within 90 days of a client request.

Brokers and consultants should be considering how these provisions may affect their broker services agreements, maybe even the need to establish formalized broker agreements if one does not exist as well as evaluating procedures for what information you need to obtain or documents to communicate compensation.

Brokers and consultants should also start to educate their clients on the new disclosure requirements and use this an opportunity to establish greater transparency and trust with the employers. The new compensation transparency disclosures will allow employers to spotlight not just how much brokers are being paid but also allow brokers to showcase how they are bringing results that help their employer clients sponsor and manage healthcare solutions and truly go beyond just delivering rate renewals.

Next Steps For Brokers

Brokers and consultants should be considering whether they want to enter into a contract with their clients, or whether they want to provide disclosures. The statute does not require a broker and consultant to enter into a formal contract. That statute does require certain written disclosures to applicable clients. Each broker and consultant should evaluate whether to provide a disclosure or enter into a formal contract.

There are numerous considerations that a broker and consultant should evaluate if they desire to enter into a formal contract. A formal contract may help to clarify and define the roles and responsibilities of each party. A broker or consultant should seek qualified legal counsel to develop a contract that is appropriate for their specific needs.

You also may want to consider including one or more of the following “stock” contract provisions: